New GST Rate Structure 2025: A Simplified Approach to Taxation in India

New GST Rate Structure 2025: A Simplified Approach to Taxation in India

On September 17, 2025, the Central Board of Indirect Taxes and Customs (CBIC) rolled out Notification No. 9/2025-Central Tax (Rate), ushering in a transformative overhaul of India’s Goods and Services Tax (GST) framework, effective from September 22, 2025. This update, stemming from the 56th GST Council meeting held on September 3, 2025, under the leadership of Union Finance Minister Nirmala Sitharaman, marks a pivotal shift toward a streamlined two-tier GST structure. With the majority of goods and services now taxed at 5% and 18%, this reform aims to simplify compliance, reduce costs for consumers, and bolster economic growth. Here’s a deep dive into what this means for businesses, consumers, and the Indian economy.

A Leaner GST Framework

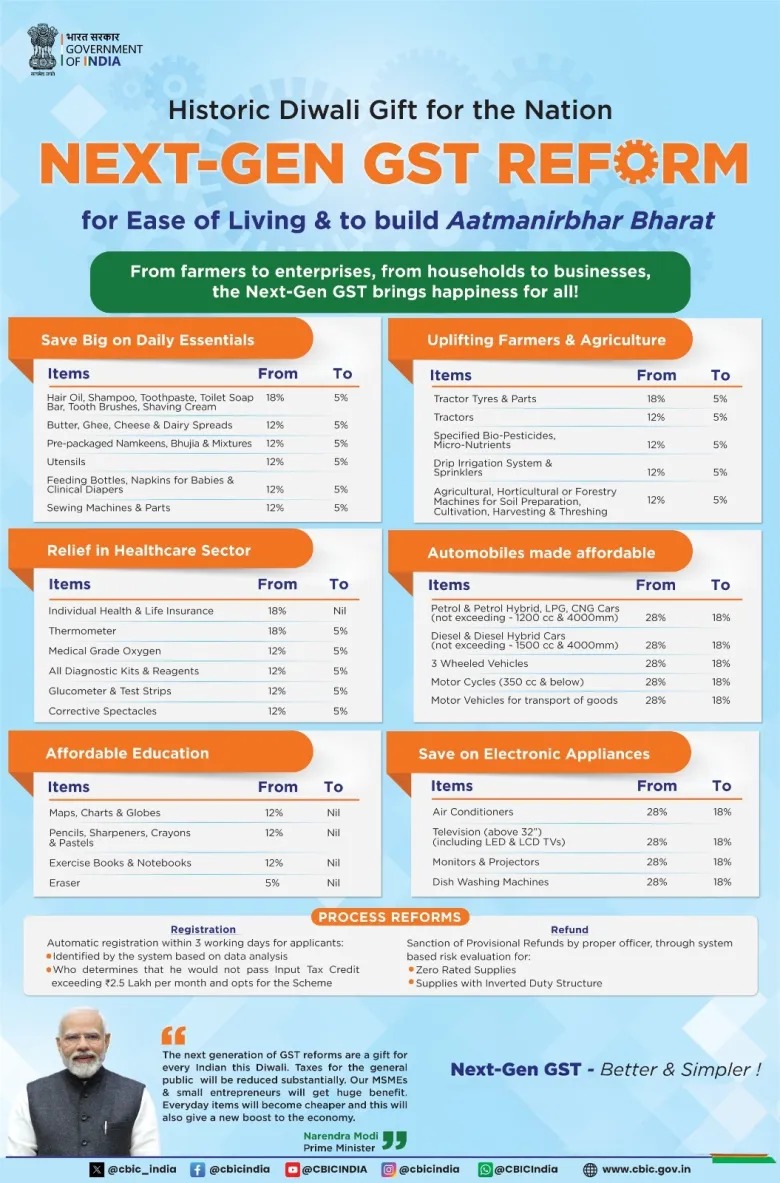

The new GST structure consolidates the previous four-slab system (5%, 12%, 18%, and 28%) into a primarily two-tier model, with rates of 5% and 18% covering most goods and services. This simplification addresses long-standing calls from industry and tax experts to reduce complexity in the GST regime. Additionally, ultra-luxury items will attract a 40% tax, while tobacco and related products remain in the 28% slab with an additional cess. Specialized rates of 0.125%, 0.75%, 1.5%, 9%, 14%, and 20% apply to specific categories, ensuring targeted relief and revenue generation.

The revised schedules, as outlined in the CBIC notification, provide clarity on applicable rates:

-

- Schedule I (2.5% CGST + 2.5% SGST = 5% GST): Covers essentials like milk products, cereals, pulses, edible oils, medicines, fertilizers, and affordable apparel/footwear (under ₹1,000).

- Schedule II (9% GST): Includes processed foods, household goods, and industrial inputs.

- Schedule III (20% GST): Targets luxury and sin goods.

- Schedule IV (1.5% GST): Offers relief for selected essentials.

- Schedule V (0.125% GST): Applies to specific precious goods like non-industrial diamonds.

- Schedule VI (0.75% GST): Covers special category goods.

- Schedule VII (14% GST): Encompasses certain high-tax items.

This restructuring aims to make taxation more predictable, reducing disputes and easing compliance for businesses.

Key Objectives of the Reform

The GST Council’s decision reflects a strategic effort to balance affordability with fiscal stability. The key goals include:

-

- Consumer Relief: Lower rates on essentials like food, medicines, and affordable clothing reduce the cost of living, particularly for low- and middle-income households.

- Simplified Compliance: A two-tier system minimizes classification errors, making it easier for businesses to determine applicable rates and file returns.

- Economic Growth: By reducing tax burdens on essential goods, the reform encourages consumption, while higher rates on luxury items ensure revenue for public welfare programs.

- Industry Efficiency: Clear rate schedules enable businesses to update pricing and supply chains swiftly, fostering transparency.

Implications for Businesses

The onus is now on industries to align their operations with the new rates. Experts emphasize the need for prompt action:

-

- System Upgrades: Businesses must update ERP systems, invoicing software, and pricing structures to reflect the new rates. This is critical for sectors dealing with diverse product categories, such as retail and manufacturing.

- Passing on Benefits: The reduction in rates, particularly for essentials, requires businesses to lower prices to benefit consumers. Failure to do so could attract scrutiny from tax authorities under anti-profiteering provisions.

- Supply Chain Adjustments: Manufacturers and distributors must ensure that input tax credits (ITC) are optimized under the new structure to avoid cost escalations.

Rajat Mohan, Senior Partner at AMRG & Associates, noted that the government’s clear schedules provide much-needed clarity, but businesses must act swiftly to ensure compliance across supply chains. Similarly, Saurabh Agarwal from EY stressed the importance of aligning pricing and logistics to pass on rate reductions to consumers, ensuring the reform’s benefits reach the end user.

Impact on Consumers

For the average Indian, the new GST structure is a boon. Essentials like milk, cereals, edible oils, and medicines, now taxed at 5%, will become more affordable, easing household budgets. Affordable footwear and apparel (under ₹1,000) also fall under the 5% slab, supporting the aspirational middle class. However, luxury goods and sin products (e.g., high-end cars, tobacco) will remain expensive, aligning with the government’s focus on taxing non-essential consumption.

The exemption of certain services, such as skill training by NSDC partners and specific insurance services, further reduces costs for education and healthcare access. These changes, combined with earlier exemptions (e.g., gene therapy, railway platform tickets), reflect a consumer-centric approach.

State-Level Implementation

Since GST revenue is shared equally between the Centre and States, states must now notify their State GST (SGST) rates to align with the new Central GST (CGST) rates. This ensures uniformity across intra-state and inter-state transactions. The CBIC’s notification provides a robust framework, including definitions like “unit container” and “pre-packaged and labelled”

(aligned with the Legal Metrology Act, 2009), to prevent misinterpretation. States are expected to issue SGST notifications promptly to avoid disruptions in tax collection.

Broader Context and Recent GST Updates

The 2025 reform builds on earlier GST Council decisions. For instance, the 55th meeting (December 2024) reduced rates on fortified rice kernels (18% to 5%), exempted gene therapy, and clarified rates for used electric vehicles. The 54th meeting (2024) lowered rates on cancer drugs (12% to 5%) and helicopter passenger transport (18% to 5% on seat-share basis). These changes demonstrate the Council’s ongoing efforts to address inverted duty structures and support critical sectors like healthcare and transportation.

The introduction of specialized rates (e.g., 0.125% for precious goods, 0.75% for special categories) also caters to niche industries, ensuring fairness without compromising revenue. The continued application of cess on sin goods (e.g., tobacco, aerated drinks) maintains fiscal discipline.

Challenges and the Road Ahead

While the simplified structure is a step forward, challenges remain:

- Compliance Burden: Small businesses may struggle to update systems by September 22, 2025, requiring support from trade bodies and tax professionals.

- Anti-Profiteering Risks: The government will monitor whether businesses pass on rate reductions, with potential penalties for non-compliance.

- Luxury Tax Implementation: The 40% rate on ultra-luxury items may face legal challenges if classification disputes arise.

The success of this reform hinges on transparent adoption by businesses and vigilant enforcement by authorities. The GST Council, supported by the Fitment Committee, will likely continue refining rates to address anomalies, such as inverted duty structures, in future meetings.

Conclusion

The new GST rate structure, effective September 22, 2025, is a landmark reform that simplifies India’s indirect tax regime while prioritizing affordability and compliance. By focusing on essentials and streamlining slabs, the government aims to benefit consumers, businesses, and the broader economy. As states align their SGST rates and industries adapt, the reform promises to enhance transparency and economic efficiency. For businesses, the key is to act swiftly; for consumers, it’s a chance to enjoy lower costs on everyday goods. Stay tuned for further updates as the GST Council continues to shape India’s tax landscape.

For the complete notification, visit the CBIC website or refer to official gazettes for detailed schedules and clarifications.